I will try to provide you with all the links, screenshots and relevant contact details where I can, some departments were more helpful than others should I say. Details were correct as of Feb 2016.

The whole process for me had two sections:

Part 1 – The NOVA form (Notification Of Vehicle Arrival) = Paying the Import and Tax Duties. (This section)

Part 2 – DVLA (Driver and Vehicle Licensing Agency) = Registering the vehicle for the UK. Click here for the link.

Each section I will try pull the relevant information for the words on the web pages. If you have the NOVA declaration then you can jump straight to Part 2 – DVLA section.

Background

This is a complete minefield I have to say as I soon found out. Nowhere on the net could I find out what I wanted to know or how I even go about getting that information. Yes there are plenty of “helpful” government websites, but they are so tied up with their own red tape it’s like trying to find a grain of salt on a sandy beach. I will try to explain what I went through as best I can and even if it points you in the right direction then at least I have helped somebody.

When I purchased my car as a project car I was unaware that you had to had a vital document called the NOVA or Notification Of Vehicle Arrival. This document proves that import and VAT taxes have been paid. Without it you can’t register the car in the UK. You may own the ownership papers, but that car is destined to sit on the drive.

The NOVA form

The NOVA certificate is a confirmation that all the duties – Import and VAT for the imported car have been paid.

First Contact

I was first advised to call the classic car import that you need to obtain the correct import code in order to pay the duties owing. Telephone – 0300 0579069

They were very helpful and pointed me to correct pages on the Government Website. Once I established the details and codes for my vehicle, I then composed a letter to the HMRC department via email to:

ecsm.nchcars@hmrc.gsi.gov.uk

That letter contained the following details.

- Make, Model and details of the car including the Vin number and previous registration number.

- How I came to purchase the car via a trader on DD/MM/YYYY and paid £xx,xx for it

- Why there is no NOVA confirmed

- Attached a copy of the Ownership papers

- Attached copy of my receipt of purchase

- The suspected code that I thought should be used for the vehicle

- My full contact details, address and email

They replied with the following letter stating the preliminary import codes that I had thought were correct I completed the form and sent that back to them. If you have any of the documents listed within this letter, then they should be copied and returned with the letter. As I had none of those forms listed I was starting from scratch.

Once the department where happy with all the details and the import codes they sent me a simple one page invoice for the amounts owing for the Import Duty and the VAT. There are multiple ways to pay as explained on their letter.

Once that has been paid in full and cleared, they will send you a very simple headed paper, single page letter to say vehicle Vin xxxxxxx number has paid all the appropriate duties. This will be stamped with your own unique reference number. For obvious reasons I can’t post those details on a blog. DO NOT LOOSE THIS DOCUMENT.

To work out the duties for yourself or what you will be expecting to pay follow these links.:

DVLA Driving home page Link – https://www.gov.uk/browse/driving

https://www.gov.uk/importing-vehicles-into-the-uk

Import of Vehicle

A completed form C384 (available to download from HMRC website)

- C88/E2 import entry paperwork(this may be also be known as a Customs entry).

https://www.gov.uk/guidance/declarations-and-the-single-administrative-document

Classification of vehicle

https://www.gov.uk/guidance/classifying-vehicles

4. VAT, duty and tax: vehicles from outside the EU

You usually pay VAT and duty through customs when you import any vehicle from outside the EU.

You must pay vehicle tax from the date your vehicle is registered with DVLA.

Report the arrival of your vehicle to HMRC

Use the Notification of Vehicle Arrivals (NOVA) service to tell HM Revenue and Customs (HMRC) you’ve brought a vehicle into the UK. (Form C88/E2)

Pay VAT and duty through customs

You must pay VAT and duty through customs when you import a vehicle, unless you’re:

- moving to the UK

- importing a previously exported vehicle

- importing a vehicle registered to a non-EU resident

If you’re moving to the UK

You don’t pay VAT or duty on a vehicle imported from outside the EU if you qualify for transfer of residence relief. To qualify you must meet all of these conditions:

- you’re moving your normal home to the UK

- your normal home was outside the EU for a continuous period of at least 12 months

- you’ve owned and used the vehicle for at least 6 months outside the EU

- you didn’t get the vehicle under a duty-free or tax-free scheme

- you’re going to keep the vehicle for your personal use for at least 12 months

To get the tax relief, fill in form C104A and give it to customs when you enter the country.

Importing previously exported vehicles

You don’t pay VAT or duty on a vehicle imported from outside the EU if it was previously exported out of the EU. This is known as ‘returned goods relief’. To qualify you must meet all of these conditions:

- you exported the vehicle outside the EU within the last 3 years

- the taxes were paid on the vehicle in the EU and not refunded when it was exported

- the vehicle hasn’t been altered outside the EU, other than necessary running repairs

To get the tax relief, drive your vehicle through the ‘green channel’. You must have proof that:

- the vehicle was exported

- you were the person who exported it

Non-EU registered vehicles

You don’t pay VAT or duty on a vehicle imported from outside the EU if it’s registered to a non-EU resident and:

- you’re not an EU resident

- you’re importing the vehicle temporarily for your own private use

- you don’t sell, lend or hire it within the EU

- you re-export it from the EU within 6 months – you get longer if you’re a student or on an assignment lasting a specific amount of time

This is known as ‘temporary admission relief’. Fill in form C110 to help customs identify you. You don’t need to contact HM Revenue and Customs (HMRC) to get the relief.

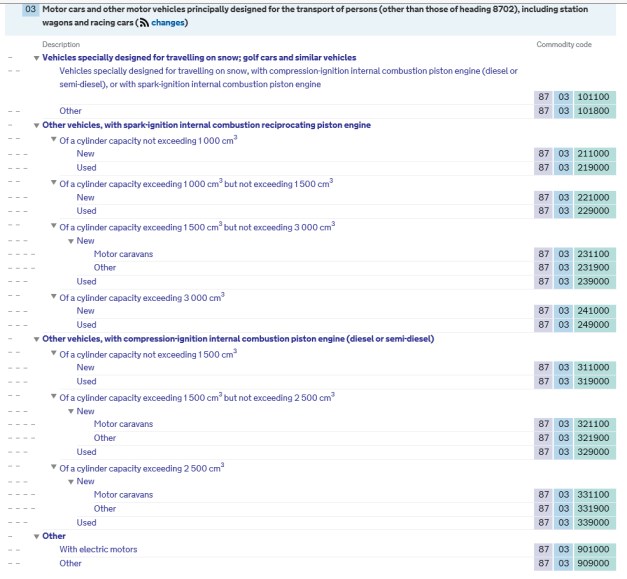

Trade Tarrifs

https://www.gov.uk/trade-tariff/sections

https://www.gov.uk/trade-tariff/chapters/87

https://www.gov.uk/trade-tariff/commodities/8703249000#import

The Tariff Classification Service

You can use the UK Trade Tariff to look up classification codes.

After looking through all the lengthy charts and tables you are still unable to self-assess your products, and you need additional support or help, you can email the team on: classification.enquiries@hmrc.gsi.gov.uk.

NOTE: You must only detail one item per email.

To ensure your enquiry is dealt with efficiently, please include the following information in your email request:

- what the product is

- what it is made of

- if it’s made of more than one material please explain the breakdown of the materials

- what it’s used for

- how the product works / functions

- how it’s presented / packaged

The products listed below will require you to provide additional information.

- footwear

include the type (shoe, boot, slipper etc.), upper material details, outer sole material details, the heel height and the purpose for men or woman - food

include precise composition details by percentage weight of all the ingredients to 100% and the method of manufacture or process undergone e.g. fresh, frozen, dried, further prepared / preserved etc - chemicals

include the Chemical Abstracts Service (CAS) number, whether the product is a liquid/powder/solid and include the percentages of the ingredients - textiles

please include the material composition, how it is constructed (knitted /woven) and the name of fabric - vehicles

please include the age, the engine type (petrol or diesel), the engine size, whether the vehicle is new or used, whether the vehicle is over 30 years old and whether it is in its original condition. Is the vehicle going to be for everyday use?

A classification officer will respond by providing you with non-legally binding classification advice based on the information you have supplied.

If you’d like customs to make a binding decision on correct classification of your goods, you should apply electronically for a Binding Tariff Information (BTI) ruling. Find out more about electronic BTI in Notice 600.

This BTI will be legally binding throughout the EU for up to 6 years after the date of issue.

BTI is usually free. You will have to pay costs incurred through laboratory analysis, obtaining expert advice and returning your samples.

BTI provides you with:

- the correct commodity code for your goods

- a detailed description of your goods, enabling any customs regime to identify them

- legal justification for the decision TCS has reached

- a unique reference number

BTI can only be obtained before any customs procedures take place. Your request may be refused altogether if you:

- don’t plan to import or export the goods in question

- have made a similar application in another EU member state

- can’t provide complete information about your goods

Enter your BTI reference number in Box 44 of the SAD which must accompany your goods throughout the EU. See declarations and the SAD.

You should complete a separate application form for each type of item you want classified.

BTI appeals

If you’re unhappy with a BTI decision you may lodge an appeal with HMRC. You have 45 days to request an independent review of the decision. If you’re unhappy with the review you have 30 days to apply for a tribunal hearing.

Find out how to apply for a review of a BTI decision in section 3 of Notice 600.

6. Registering a vehicle as ‘new’

You can bring a vehicle into the UK and register it as ‘new’ if all the following apply:

- it’s registered within 2 weeks of collection (extended to one calendar month at peak periods, eg before 1 March and 1 September)

- it hasn’t been previously permanently registered

- it’s been stored before registration and is a current model or a model that’s stopped being made within the last 2 years

- it only has reasonable delivery mileage, eg it’s been driven from the pickup point to home using a direct route

- it hasn’t been sold by a retailer before

You can’t drive the vehicle on UK roads until it’s been registered and taxed, unless you’re driving to a pre-booked MOT or type approval test.

So now in theory you will have the NOVA form to prove that you have legally imported and paid the correct duties for your vehicle.

MY DISCLAIMER:

I will take no responsibility for using my guide set out below or be liable for any damages / loss as a result of using this guide. Please use your judgement and follow the procedures as required by the agencies involved and by law. All details have been changed for documentation purposes or removed for obvious reasons as this is a guide only.